The U.S. Senate passed the Infrastructure Investment and Jobs Act on a broad bipartisan vote of 69-30. This historic bill includes many of President Joe Biden’s economic priorities, including record investments in minority-owned businesses, broadband infrastructure, expanded funding to track and address climate change, while also including the largest-ever federal investments in roads and bridges, clean drinking water and more.

After the Senate passed the Infrastructure Investment and Jobs Act, U.S. Secretary of Commerce Gina M. Raimondo released the following statement:

“I am deeply thankful for the unwavering commitment of the Republican and Democratic Senators who led the process to get this done. Throughout the entire process, President Biden showed incredible leadership keeping these talks together and encouraging all of us to remain committed to this bipartisan approach. Passing a bipartisan infrastructure bill sends a message to nations around the world about the strength of our democracy and what we can accomplish together for the benefit of all Americans. The investments in this bill will better position the United States to compete globally, strengthen our supply chains, and create millions of good-paying jobs – all while making our economy more resilient and just.

“The Infrastructure Investment and Jobs Act represents a historic investment in our country that will strengthen our economy to benefit all Americans for decades to come. This is a generational achievement that both parties can be proud of, and there is still more to do as we carry out President Biden’s Build Back Better agenda. Broad support exists to make needed investments in the Care Economy to provide access to affordable, quality care services as well as reinvigorating workforce training to ensure our workers are prepared for the jobs of the 21st century. I look forward to continued engagement with Congress to make progress on these critical challenges.”

Among the historic investments included in the bill is more than $48 billion in funding for the National Telecommunications and Information Administration (NTIA) to fund state and local investments to help reach 100% access to affordable, high-speed broadband service. This is among the most significant government investment in broadband access and infrastructure in American history, and is a critical component of President Biden’s Build Back Better agenda.

The bill will also make permanent the Minority Business Development Agency (MBDA), enhancing its ability to promote and administer its flagship programs to promote the growth, development, and resiliency of minority-owned businesses. As the only federal agency dedicated solely to economic development for minority businesses, the move to permanently authorize MBDA is essential to ensuring the economic recovery reaches all of America’s communities.

Finally, the legislation makes major investments to tackle climate change, increase infrastructure resiliency, and restore and improve coastal habitats by providing the National Oceanic and Atmospheric Administration (NOAA) with approximately $3 billion in funding for climate science and services.

U.S. Customs and Border Protection (CBP) is adjusting certain customs user fees and corresponding limitations established by the Consolidated Omnibus Budget Reconciliation Act (COBRA) for Fiscal Year 2022 in accordance with the Fixing America's Surface Transportation Act (FAST Act) as implemented by the CBP regulations.

The adjusted amounts of customs COBRA user fees and their corresponding limitations set forth in this notice for Fiscal Year 2022 are required as of October 1, 2021.

I. Background

A. Adjustments of COBRA User Fees and Corresponding Limitations for Inflation

On December 4, 2015, the Fixing America's Surface Transportation Act (FAST Act, Pub. L. 114-94) was signed into law. Section 32201 of the FAST Act amended section 13031 of the Consolidated Omnibus Budget Reconciliation Act (COBRA) of 1985 (19 U.S.C. 58c) by requiring the Secretary of the Treasury (Secretary) to adjust certain customs COBRA user fees and corresponding limitations to reflect certain increases in inflation.

Sections 24.22 and 24.23 of title 19 of the Code of Federal Regulations (19 CFR 24.22 and 24.23) describe the procedures that implement the requirements of the FAST Act. Specifically, paragraph (k) in § 24.22 (19 CFR 24.22(k)) sets forth the methodology to determine the change in inflation as well as the factor by which the fees and limitations will be adjusted, if necessary. The fees and limitations subject to adjustment, which are set forth in appendix A and appendix B of part 24, include the commercial vessel arrival fees, commercial truck arrival fees, railroad car arrival fees, private vessel arrival fees, private aircraft arrival fees, commercial aircraft and vessel passenger arrival fees, dutiable mail fees, customs broker permit user fees, barges and other bulk carriers arrival fees, and merchandise processing fees, as well as the corresponding limitations.

B. Determination of Whether an Adjustment Is Necessary for Fiscal Year 2022

In accordance with 19 CFR 24.22, CBP must determine annually whether the fees and limitations must be adjusted to reflect inflation. For Fiscal Year 2022, CBP is making this determination by comparing the average of the Consumer Price Index—All Urban Consumers, U.S. All items, 1982-1984 (CPI-U) for the current year (June 2020-May 2021) with the average of the CPI-U for the comparison year (June 2019-May 2020) to determine the change in inflation, if any. If there is an increase in the CPI-U of greater than one (1) percent, CBP must adjust the customs COBRA user fees and corresponding limitations using the methodology set forth in 19 CFR 24.22(k). Following the steps provided in paragraph (k)(2) of § 24.22, CBP has determined that the increase in the CPI-U between the most recent June to May twelve-month period (June 2020-May 2021) and the comparison year (June 2019-May 2020) is 1.94 percent. As the increase in the CPI-U is greater than one (1) percent, the customs COBRA user fees and corresponding limitations must be adjusted for Fiscal Year 2022.

C. Determination of the Adjusted Fees and Limitations

Using the methodology set forth in § 24.22(k)(2) of the CBP regulations (19 CFR 24.22(k)), CBP has determined that the factor by which the base fees and limitations will be adjusted is 11.009 percent (base fees and limitations can be found in appendices A and B to part 24 of title 19). In reaching this determination, CBP calculated the values for each variable found in paragraph (k) of 19 CFR 24.22 as follows:

The arithmetic average of the CPI-U for June 2020-May 2021, referred to as (A) in the CBP regulations, is 261.992;

The arithmetic average of the CPI-U for Fiscal Year 2014, referred to as (B), is 236.009;

The arithmetic average of the CPI-U for the comparison year (June 2019-May 2020), referred to as (C), is 257.092;

The difference between the arithmetic averages of the CPI-U of the comparison year (June 2019-May 2020) and the current year (June 2020-May 2021), referred to as (D), is 4.900;

This difference rounded to the nearest whole number, referred to as (E), is 5;

The percentage change in the arithmetic averages of the CPI-U of the comparison year (June 2019-May 2020) and the current year (June 2020-May 2021), referred to as (F), is 1.94 percent;

The difference in the arithmetic average of the CPI-U between the current year (June 2020-May 2021) and the base year (Fiscal Year 2014), referred to as (G), is 25.984; and

Lastly, the percentage change in the CPI-U from the base year (Fiscal Year 2014) to the current year (June 2020-May 2021), referred to as (H), is 11.009 percent.

D. Announcement of New Fees and Limitations

The adjusted amounts of customs COBRA user fees and their corresponding limitations for Fiscal Year 2022 as adjusted by 11.009 percent set forth below are required as of October 1, 2021. Table 1 provides the fees and limitations found in 19 CFR 24.22 as adjusted for Fiscal Year 2022, and Table 2 provides the fees and limitations found in 19 CFR 24.23 as adjusted for Fiscal Year 2022.

Table 1—Customs COBRA User Fees and Limitations Found in 19 CFR 24.22 as Adjusted for Fiscal Year 2022

Limitation: Maximum Express Consignment Carrier/Centralized Hub Facility Fee

1.11

(a)(9)(B)(i); (b)(8)(A)(i)

(b)(1)(i)(B)

Limitation: Minimum Merchandise Processing Fee

27.75

(a)(9)(B)(i); (b)(8)(A)(i)

(b)(1)(i)(B)

Limitation: Maximum Merchandise Processing Fee

538.40

(b)(8)(A)(ii)

(b)(1)(ii)

Fee: Surcharge for Manual Entry or Release

3.33

(a)(10)(C)(i)

(b)(2)(i)

Fee: Informal Entry or Release; Automated and Not Prepared by CBP Personnel

2.22

(a)(10)(C)(ii)

(b)(2)(ii)

Fee: Informal Entry or Release; Manual and Not Prepared by CBP Personnel

6.66

(a)(10)(C)(iii)

(b)(2)(iii)

Fee: Informal Entry or Release; Automated or Manual; Prepared by CBP Personnel

9.99

(b)(9)(A)(ii)

(b)(4)

Fee: Express Consignment Carrier/Centralized Hub Facility Fee, Per Individual Waybill/Bill of Lading Fee

1.11

Tables 1 and 2, setting forth the adjusted fees and limitations for Fiscal Year 2022, will also be maintained for the public's convenience on the CBP website at www.cbp.gov.

Troy A. Miller, the Acting Commissioner, having reviewed and approved this document, is delegating the authority to electronically sign this notice document to Robert F. Altneu, who is the Director of the Regulations and Disclosure Law Division for CBP, for purposes of publication in the Federal Register.

The Congressional Research Service (CRS) of the US Library of Congress has issued a report with an overview of current information reporting requirements, as well as policy proposals and consideration, for certain cryptocurrency transfers. The CRS report is entitled "Cryptocurrency Transfers and Data Collection" (IF11910, 25 August 2021).

For US federal tax purposes, taxpayers should treat cryptocurrency transactions in the same manner as transactions involving other mediums of value, such as cash, checks and stocks. Accordingly, cryptocurrency transactions are subject to the capital gains and losses rules of the US Internal Revenue Code (IRC). Similarly, US federal income and employment tax rules apply when a business uses cryptocurrency to compensate an individual for a service provided. Cryptocurrency transactions are also generally subject to the same information reporting requirements as non-cryptocurrency transactions.

The Biden Administration's fiscal year (FY) 2022 Budget proposes:

requiring cryptocurrency exchanges and custodians to file information returns with the US Internal Revenue Service (IRS) that report the amount flowing into and out of customer accounts with gross flows above USD 600 with a separate reporting requirement for inter-broker cryptocurrency transfers;

requiring businesses that accept cryptocurrency to report crypto transactions exceeding USD 10,000 in value to the IRS; and

expanding the information reporting requirements for brokers, including cryptocurrency exchanges and wallet providers, to include information on US and certain foreign account owners to allow for automatic information sharing with foreign tax jurisdictions in exchange for information on US taxpayers transacting in cryptocurrency outside the United States.

The Infrastructure Investment and Jobs Act (H.R. 3684), as passed by the US Senate on 10 August 2021 would, if enacted:

require a party facilitating the transfer of cryptocurrency to file an information return as a broker with the IRS; and

require a business that receives cryptocurrency worth more than USD 10,000 in a single transaction to report the transaction to the IRS.

The CRS report notes that US policymakers face a trade-off between providing the necessary tools to ensure anti-money laundering (AML) compliance and driving activities out of the US market because cryptocurrency can be used across jurisdictions with relative ease.

Note: The CRS is an agency within the US Library of Congress and serves the US Congress throughout the legislative process by providing legislative research and analysis for an informed national legislature.

To level the playing field and address the concerns of small business owners, President Biden's plan, if adopted by the US congress, will:

raise the corporate income tax rate from 21% to 28%;

strengthen the global minimum tax for large multinational corporations;

reduce incentives for foreign jurisdictions to maintain ultra-low corporate tax rates by encouraging global adoption of robust minimum taxes for large corporations;

enact a 15% minimum tax on book income of large, highly profitable corporations;

eliminate incentives for large corporations to offshore profits and jobs;

ramp up enforcement to address tax avoidance among large corporations;

extend the expansion of the Child Tax Credit (CTC) in the American Rescue Plan Act (ARP) (from USD 2,000 per child to USD 3,000 per child for children over the age of six and USD 3,600 for children under the age of six); and

permanently extend the tax credits that lowered health insurance premiums for those buying coverage through the Affordable Care Act (ACA) (www.HealthCare.gov).

The Fact Sheet states that, according to the US Treasury Department's analysis, President Biden's plan will protect 97% of small business owners from income tax rate increases while delivering tax cuts to more than 3.9 million entrepreneurs.

The federal tax gap is a measure of taxpayer non-compliance. The US Internal Revenue Service (IRS) provides two estimates of the tax gap:

the gross federal tax gap, i.e. the difference between:

the total amount of federal individual and corporate income, employment, and estate and gift taxes owed in a year; and

the total amount of those taxes paid voluntarily in full and on time; and

the net tax gap, i.e. the difference between:

all taxes owed; and

taxes paid after late taxpayer payments and taxes collected through IRS enforcement actions.

The federal tax gap has three components:

the understatement of tax liability through underreporting of income or overstating deductions, credits and other income adjustments;

the failure to pay the full amount of taxes owed when filing a tax return on time (tax underpayment); and

the failure to file a required return on time (non-filing).

The CRS report includes the following table showing the net federal tax gap from 2001 to 2013:

Years

Current USD

Constant 2020 USD

Net Taxpayer Non-compliance Rate*

2001

290 billion

423 billion

13.7%

2006

385 billion

493 billion

14.5%

2008-2010

406 billion

491 billion

16.3%

2011-2013

381 billion

431 billion

14.2%

* The percentage of total taxes owed in a year that were not paid in full and on time after IRS enforcement actions.

An updated estimate from the IRS is unlikely to be released before 2022. In testimony given at a congressional hearing in April 2021, IRS Commissioner Charles Rettig stated that the current gross federal tax gap could total as much as USD 1 trillion, although not everyone agrees with that assessment.

The CRS report states that options for decreasing the federal tax gap include:

increasing the IRS's resources, especially for enforcement;

regulating paid tax preparers;

requiring new information reporting for certain taxpayer transactions with banks;

major new investments in the IRS's information technology and employee training;

a greater emphasis on the IRS's taxpayer services;

a redesign of the IRS's information systems;

simplifying the federal tax code to make it possible for more taxpayers to meet their tax obligations on their own with fewer errors; and

clarifying ambiguous areas of the tax code to make it harder for corporations and high-income individuals to prevail in disputes with the IRS over the legality of their tax minimization strategies.

Note: The CRS is an agency within the US Library of Congress and serves the US Congress throughout the legislative process by providing legislative research and analysis for an informed national legislature.

New York has enacted legislation expanding its definition of receipts for sales and use tax purposes. The definition now includes consideration received by a vendor from third parties in certain circumstances (A01143-A / S06301). The new law is effective for sales occurring on or after 1 December 2021.

The newly enacted legislation provides that receipts shall include consideration received by the vendor from third parties under the following conditions:

the vendor receives consideration from a third party and the consideration is directly related to a rebate, discount or similar price reduction on the sale (except sales of motor vehicles);

the vendor has an obligation to pass the consideration through to the purchaser in the form of a price reduction;

the amount of the consideration to be paid by the third party is fixed and determinable by the vendor at the time of the sale of the property or service to the purchaser; and

one of the following criteria is met:

the purchaser presents to the vendor a coupon, certificate or other documentation to claim a price reduction granted by a third party, who will reimburse any vendor to whom the document is presented;

the purchaser presents identification as a member of a group or organization entitled to a price reduction (excluding the presentation of a customer loyalty or related rewards program card); or

the invoice received by the purchaser or a coupon, certificate or other documentation presented by the purchaser identifies the price reduction as third-party.

The New York Governor signed the bill into law on 20 August 2021.

On 13 August 2021, the Swiss Federal Tax Administration published a clarification, announcing that the conditions for the activation of the most favoured nation (MFN) clause contained in the amending protocol, signed on 30 August 2010, to the India - Switzerland Income Tax Treaty (1994) have been met.

The MFN clause should apply as of 1 January 2021. If India does not apply the clause on a reciprocal basis, Switzerland will apply the reduced rate from 1 January 2023.

Currently, the treaty provides for a 10% withholding tax on dividends.

The MFN clause of article 11 of the 2010 protocol provides that this rate will be reduced when India afterwards signs a new treaty with another OECD Member States providing for a lower rate.

On 29 July 2021, the Inland Revenue Department (IRD) of Hong Kong set up a webpage to provide general guidance on the IRD's approach in handling tax issues arising from the COVID-19 pandemic, including issues on the tax residence status of companies and individuals, permanent establishments, employment income of cross-border employees and transfer pricing. The IRD stresses that the treatment of each case will be determined based on its facts and circumstances.

Hong Kong’s total merchandise trade in 2020 decreased by 2.5% to US$1,051 billion (HK$8,197 billion) after dropping by 5.4% in 2019.

Hong Kong handles a large amount of offshore trade, estimated by the Hong Kong government to have a value of US$604 billion (HK$4,709 billion) in 2019, an decrease of 2.5% over 2018. In comparison, re-exports amounted to US$505 billion (HK$3,941 billion) in 2019, down 4.2% over 2018.

As of December 2020, 438,964 people were employed in the import and export sector, which had 105,675 establishments. In 2019, the sector accounted for 16.8% of Hong Kong’s GDP.

Hong Kong handles a good portion of mainland China's external trade. In 2020, about 10.1% of the mainland's exports (valued at US$263 billion) and 14.3% of imports (US$295 billion) were handled via Hong Kong and 53% of Hong Kong's re-exports originated from the mainland.

Industry DataImport and Export Trade

December 2020

Number of Establishments

105,675

Employment

438,964

Source: Quarterly Report of Employment and Vacancies Statistics, Census and Statistics Department

Exports of Merchanting and Trade-related Services (US$ billion)

2015

2016

2017

2018

2019

Exports of Merchanting and Trade-related Services

36.4

36.6

38.7

40.6

39.7

Year-on-year growth

-3.0%

+0.6%

+5.8%

+5.4%

-2.2%

Contribution to Services Exports

27.0%

28.3%

28.1%

27.4%

29.3%

Sources: Gross Domestic Product (Quarterly), Census and Statistics Department

Range of Services

Hong Kong's import and export trading firms are active in sourcing various industrial goods, including raw materials, machinery and parts, and a wide range of consumer goods. There are three main types of sourcing activities: (1) sourcing goods produced in Hong Kong; (2) sourcing goods from around the region for re-export; and (3) sourcing goods from one country to be shipped directly to a third country without touching Hong Kong territory.

The import business of Hong Kong trading firms is mainly managed by distribution through agents or dealers. These trading firms usually specialise in one product area and represent one or more foreign brands. Their trading map usually encompasses Hong Kong, mainland China (or certain parts of it) and/or other Asian countries.

With the development of trade support services in mainland China, trading firms increasingly source goods offshore for sale to international markets. Some of these goods are either transhipped via Hong Kong or shipped directly without touching Hong Kong territory. Such offshore trade is not reflected in Hong Kong's trade statistics. According to official statistics, Hong Kong's offshore trade in 2019 (including both “merchanting” and “merchandising for offshore transactions”) was estimated to be US$604 billion (HK$4,709 billion), an decrease of 2.5% over 2018. In comparison, re-exports totalled US$505 billion (HK$3,941 billion) in 2018, down 4.2% over 2018, representing 83.7% of total offshore trade.

Service Providers

Hong Kong's import and export trading firms are typically small, employing less than 10 persons on average. There were 105,675 import and export trading firms in Hong Kong as of December 2020, with the majority of them being SMEs. There are three broad categories of import and export trading firms:

Left hand-right hand traders: these refer to trading firms which match sellers and buyers without adding any significant value to the process. These firms conduct a straight-forward sourcing operation, usually identifying goods produced on the mainland or Hong Kong and shipping them to overseas markets. They rely on their specialist knowledge of the sources of products in the region and the low costs of their supplies as their main competitive advantages.

Traders with some value-added services: many firms now source raw materials for their suppliers and provide finance for these materials. They often use letters of credit from their customers as a guarantee for raising finance for their purchase orders. Other firms develop a sub-contractor relationship with a number of factories in which they exert significant control over the management of production, including quality control.

Traders with sophisticated value-added services: in certain cases exporting firms have added value to their traditional activity to such an extent that it may be difficult to retain the label of being exporters. For example, some firms design and manufacture components for their supplier factories to produce finished goods, which the firms subsequently export. These firms add value mostly from their design team, and their competitive edge comes from their ability to design products which sell well in the target markets. In 2019, the rate of gross margin1 of merchanting fell slightly to 6.3% from 6.4% in 2018. This means that the export market is relatively stable, though margins remain below the 6.9% recorded in 2009. In the same year, the commission rate of merchandising2 for offshore transactions stood at 6.2% (2018:6.7%; 2017: 6.9%).

The business environment for Hong Kong's trading firms is becoming more challenging amid the growing trend toward direct dealing between customers and manufacturers, known as “trade disintermediation”. In response to this, Hong Kong traders are adapting to provide more value-added services, in addition to finding more competitive sources of supplies. For example, Hong Kong traders help their overseas clients to inspect the goods produced by the manufacturers to ensure they meet the procurement standard, and monitor production schedules to meet delivery. Hong Kong traders can also help overseas buyers co-ordinate production when the buyers have a sudden surge in orders and quick turnaround is needed.

The operations of small and big trading firms are quite different. Smaller firms are usually strong in introducing foreign products to the mainland market. In most cases, they specialise in one area, such as medical equipment, and represent some foreign brands as their agents or distributors. Bigger trading firms are usually strong in sourcing products from the region. They usually have regional or even global sourcing networks and do not specialise in just one type of product.

Exports

Hong Kong's import and export trading sector provides services mainly in the form of offshore buying and selling of goods. Given Hong Kong's location and the relocation of Hong Kong's manufacturing bases to the mainland, particularly the Pearl River Delta, mainland China is a major source of offshore trading activities. Hong Kong manufacturers are diversifying their production activities to other low-cost countries, and the offshore trading pattern is expected to reflect this move. In 2019, Hong Kong earned US$39.7 billion from exporting merchanting and trade-related services, accounting for 29.3% of total services exports.

Industry Development and Market Outlook

Impacted by the Covid-19 pandemic and the softening of global demand, Hong Kong’s total merchandise trade decreased by 2.5% to US$1,051 billion (HK$8,197 billion) in 2020, after dropping by 5.4% in 2019. In the same period, Hong Kong’s merchandise exports saw a year-on-year decrease of 1.5%, after a fall of 4.1% in the previous year. In 2020, Hong Kong's major export markets were mainland China (59.2% of total), the ASEAN (7.2%) and the EU (7.1%).

In recent years, Asia has become a more integrated market, thanks to the various free trade agreements (FTAs) signed in the region. In particular, the product trade arrangements under the China-ASEAN Free Trade Area (CAFTA) pact, which commenced in 2005 with scheduled tariff elimination completed in 2010, have contributed to higher intra-Asian trade. In November 2015, China and ASEAN concluded an upgraded FTA that covers further liberalisation of trade as well as economic, investment and regulatory co-operation. The upgraded protocol of the CAFTA took effect on 22 October 2019.

Over the past few years, there has been an increase in companies in developed economies treating Asia as a market instead of a pure production base. During 2015-2020, North America’s exports to Asia expanded by a CAGR of 1.1%, surpassing the CAGR of 1.0% in respect of its exports to Europe in the same period.

ASEAN as a group is the second largest export market and second largest trading partner of Hong Kong, with Singapore, Vietnam and Thailand being the top three markets for Hong Kong products in 2020. To foster stronger economic ties between Hong Kong and ASEAN, the two sides signed the Hong Kong-ASEAN Free Trade Agreement (HAFTA) in November 2017. In addition to the reduction and/or elimination of import tariffs, other key elements covered by the HAFTA include rules of origin, liberalisation of trade in services, promotion and protection of investment, and intellectual property co-operation. Part of the HAFTA entered into force in June 2019.

The 14th Five‑Year Plan was announced in March 2021, with an emphasis on expanding domestic demand, accelerating the domestic circulation and “dual circulation” development strategy, improving the business environment, and promoting further economic growth. As an international trade center, Hong Kong companies can actively expand the mainland domestic market under the internal circulation, while playing an important role in the cross-border trade under the external circulation, bringing new business opportunities for Hong Kong’s trade sector.

CEPA ProvisionsThe Mainland and Hong Kong Closer Economic Partnership Arrangement (CEPA) is a free trade agreement concluded by the mainland and Hong Kong. Under CEPA, all products of Hong Kong origin, except for a few prohibited articles, can be imported into the mainland tariff-free. In the services sector, Hong Kong service suppliers (HKSS) can provide, in the form of wholly owned operations, commission agents' services and wholesale trade services, and can set up wholly owned external trading companies in mainland China.

After 10 annual supplements signed between 2004 and 2013 to keep widening and broadening the liberalisation measures in favour of HKSS, Hong Kong and the mainland entered into a subsidiary agreement under CEPA in 2014 to achieve basic liberalisation of trade in services in Guangdong (Guangdong Agreement). This was followed by the Agreement on Trade in Services (ATIS) to extend the coverage of the 2014 agreement from Guangdong to the rest of the mainland from June 2016. Unlike the previous supplements which adopted a positive-list approach to introducing liberalisation measures, the two latest CEPA agreements adopt a hybrid approach to granting preferential access to Hong Kong using both positive and negative lists. From June 2020 onwards, the Agreement Concerning Amendment to the CEPA Agreement on Trade in Services (Amendment Agreement) signed in November 2019 takes effect. The Amendment Agreement introduces more liberalisation measures, including the removal of a minimum capital input ratio requirement and the relaxation of qualification requirements in a number of important services sectors. With this enhanced liberalisation of trade in services between mainland China and Hong Kong, the territory’s status as an international trade hub as well as the gateway to the mainland is set to strengthen. Please click to view further information on the latest CEPA agreements.

1 “Rate of gross margin” refers to the gross margin from merchanting expressed as a percentage of the sales value of goods involved, while “commission rate” is the commission from merchandising for offshore transactions expressed as a percentage of the sales value of goods involved. “Rate of re-export margin” is defined as the re-export margin expressed as a percentage of the value of re-exports.

2 The difference between “merchanting” and “merchandising” is that an establishment engaged in “merchanting” takes ownership of the goods involved, whereas one engaged in merchandising transactions does not take ownership of the goods involved.

As part of continuous efforts to improve the business environment, mainland China recently further streamlined foreign trade approval across the country and in free trade zones. Hong Kong companies can establish Hong Kong-funded import-export enterprises in the China (Guangdong) Pilot Free Trade Zone and start trading there without first seeking approval or completing record filing formalities. Tapping import and export trade opportunities in the Guangdong-Hong Kong-Macao Greater Bay Area (GBA) will facilitate further exploitation of mainland China’s huge domestic market.

Reform and opening-up

Mainland China has been promoting business systems reform and streamlining administrative approval procedures to attract Hong Kong companies and other investors to do business on the mainland in recent years. One effective way to tap the mainland market potential is to set up a domestic sales or import-export company there.

Guangdong lies adjacent to Hong Kong and is connected by convenient transport and logistic networks. Its position as an important industrial production and product procurement base makes it easy for companies to map out development and cargo transportation plans according to their business situation, ship goods to Hong Kong and other overseas markets, or to sell overseas goods into the mainland. Setting up a Hong Kong-funded enterprise in Guangdong is an important window for entering the mainland, one that opens opportunities for tapping the huge GBA market for domestic sales and import-export trade.

Hong Kong companies may consider going to the Guangdong Free Trade Zone to explore trade opportunities in the GBA.

Hong Hong Kong businesses can sell overseas goods to the mainland to tap the domestic market.

According to the Foreign Trade Law of the People’s Republic of China, foreign trade operators engaged in the import and export of goods or technology must register for record filing purposes with the administrative department of foreign trade at the State Council or the institution entrusted thereby. Based on the Measures for Registration and Filing of Foreign Trade Operators, they are required to use the Ministry of Commerce unified business system platform to apply for record filing and registration as foreign trade operators. The mainland customs authorities will process the relevant customs declaration and release procedures for the enterprise’s goods import or export after application approval.

In July this year, the Ministry of Commerce released an implementation plan [1] aimed at deepening reform in separating business licences and operation permits and further stimulating the development of market vitality. It is worth noting that in the section on record filing and registration of foreign trade operators it is further stated that approval is replaced by record filing across the country. A highlight in this plan is that the competent department shall initiate filing procedures and will not make a decision to deny filing once an enterprise has submitted the required filing materials. The enterprise may proceed with import-export business after completing the filing and registration procedures.

Hong Kong companies can take advantage of Guangdong’s leading edge in manufacturing, logistics and transportation and the nationwide reform of record filing for foreign trade operators to develop import and export business on the mainland by setting up companies in Guangdong.

Scrapping approvals

Apart from the nationwide reform mentioned above, the implementation plan further deepens the pilot reform in free trade zones by scrapping approval requirements for foreign trade operators outright. Between 1 December 2019 and 30 November 2022, enterprises registered within the free trade zones for import and export activities are no longer required to complete record filing and registration formalities for foreign trade operators before importing or exporting goods. Nor are they required to submit materials on the record filing and registration of foreign trade operators for customs clearance to customs offices before staring operations.

These measures have greatly simplified the registration procedures for foreign trade business. In the Guangdong Free Trade Zone, for instance, Hong Kong-funded enterprises established within the zone, whether in the Nansha Area of Guangzhou, the Qianhai-Shekou Area of Shenzhen, or the Hengqin Area of Zhuhai, may start import-export business once they are issued the business licence. Scrapping foreign trade operator record filing and registration formalities saves companies time and cost from incorporation to actual commencement of import and export activities.

In June this year, the Guangdong provincial government also released its own implementation plan for deepening the reform of separating business licences and operation permits [2], putting forward measures to improve the efficiency of enterprises in the province. These measures, including the easing of domicile (place of business) restrictions and the simplification of proof of domicile requirements, make it more convenient for businesses to invest and operate in Guangdong. Hong Kong companies may make use of the free trade zone policy advantages and Guangdong’s business reform measures to start import and export business in the Guangdong Free Trade Zone.

Record filing formalities streamlining for foreign trade operators across the country, and the outright scrapping of foreign trade approval in the free trade zones make it much easier for Hong Kong companies to venture into the mainland for domestic sales and import-export trade. The release of the Outline Development Plan for the Guangdong-Hong Kong-Macao Greater Bay Area was followed by the introduction of measures to facilitate the launch of new business in the GBA for the benefit of investors. Using the Guangdong Free Trade Zone as a foothold, Hong Kong companies can exploit the resource advantages of the GBA to further tap potential business opportunities in the GBA market.

In May 2021, industrial production in Bulgaria grew by 15.1 per cent compared to May 2020, reads the latest Monthly Report on Bulgarian Economy released by the Economy Ministry on Thursday. Growth continued to be driven by the manufacture of motor vehicles, trailers and semi-trailers, of machinery and equipment, and of metal products.

The report, elaborated by the Economic and Financial Policy Department, presents the latest developments of main macroeconomic indicators based on statistical data as at July 16.

In May 2021 year-on-year, the industrial turnover from the export of basic metals and energy goods increased, while electricity, gas, steam and air conditioning supply contributed the most to domestic turnover growth. The growth in construction production slowed down significantly and a decline was registered in building construction. At the same time, the growth of retail trade turnover was 24 per cent, with an increasing contribution of retail sale of food, beverages and tobacco.

According to the National Employment Agency's data, the registered unemployed numbered 170,716 at the end of June, similarly to the same month of 2018 and 2019, which is a historic low for this parameter so far. The Finance Ministry's analysts expect the downward trend in the dynamics of the registered unemployed to continue in July, followed by a reversal of the trend in the fall months, mostly due to seasonal factors.

In June, the monthly Harmonised Indices of Consumer Prices (HICP) inflation rate was 0 per cent, while the annual HICP inflation rate accelerated marginally to 2.4 per cent largely yjnks to the increase in prices of energy and transport fuels in particular, as the latter reached 24 per cent year-on-year. Core inflation decelerated by 0.1 percentage points to 1.4 per cent.

The rising international prices continued to push up nominal growth in trade with goods in April. Export and import increased by 49.6 per cent and 56 per cent, respectively, from April 2020. Trade with the EU had the highest contribution to the nominal growth.

Gross external debt reached 59.1 per cent of projected GDP at end-April. It increased by 0.5 percentage points from a month earlier, driven mostly by higher short-term bank credit.

Private sector credit growth accelerated further in May, up by 6.4 per cent year-on-year, compared to an annual increase by 6.1 per cent at the end of April.

At еnd-May, a deficit of 0.1 per cent of projected GDP was reported on the Consolidated Fiscal Program (CFP). In January-May 2021, CFP receipts increased by 16.1per cent year-on-year.

At end-May, government debt amounted to 24.5 per cent of projected GDP, compared to 21 per cent of GDP a year earlier.

A proposal was submitted to the Bulgarian parliament by its members for the application of a reduced 9% VAT rate for certain medicinal products. Currently, they are subject to the standard 20% VAT rate. These products, including medical devices and dietary foods for medical purposes, are listed in Article 262 of the Law for the Medicinal Products in Human Medicine and are paid with funds from the budget of the National Health Insurance Fund.

The full text of the proposal, issued on 30 July 2021, is available here (in Bulgarian only).

As a next step, the parliament will vote on the proposal.

In January-May 2021, Bulgarian export to the EU increased by 23/4 per cent from this time last year, reaching a total of 17,616.9 million leva, according to snap statistics by the National Statistical Institute released Thursday. In May alone, the export to the EU increased by over a third, 31.4 per cent, from this time last year, to a total of 3,363.2 million leva.

EU export to Bulgaria in January-May 2021 went up by 25 per cent from the same period of 2020, reaching 17,879.5 million leva. Value-wise, the biggest import was from Germany, Romania, Italy, Greece, the Netherlands and Hungary. In May alone, the export grew by 50.4 per cent from this time last year, reaching 3,682.7 million leva.

Bulgaria ran a deficit of 262.6 million leva (FOD export - CIF import) in its foreign trade in January-May.

Trade with third countries

The Bulgarian export to third countries (non-EU members) increased by 14.4 per cent from a eyear earlier, to a total of 10,580.7 million leva. In June alone, the export to this countries grew by 26.8 per cent to 1,838.6 million leva.

Imports from third countries in January-June 2021 rose by 24.2 per cent from this time last year to 13,970.7 million leva. The biggest imports were from Turkey, the Russian Federation, China and Ukraine. In June alone, imports grew by 44 per cent to 2,690 million leva.

Trade with third countries showed a deficit of 3,390 million leva for Bulgaria in January-June, including a deficit of 851.4 million leva in June alone.

A proposal was submitted to the Bulgarian parliament by its members for the application of a reduced 9% VAT rate to supplies of fruit and vegetables. The main objective of the introduction is to reduce tax fraud in the sector.

The temporary measure would be applicable between 1 January 2022 and 31 December 2023.

The full text of the proposal, issued on 26 August 2021, is available here (in Bulgarian only).

As a next step, the parliament will vote on the proposal.

Value of the African Development Bank's recently launched 5-year Global Benchmark bond, its second of the year. With this latest issue, the bank continues to carry out its funding strategy of issuing large liquid benchmark transactions

(AfDB)

35%

Stake in container terminal port operator Marsa Maroc that the Moroccan government plans to sell to Groupe Tanger Med, operator of the Mediterranean's largest port. The sale is part of the state's efforts to manage its budget deficit and overhaul state-owned enterprises through privatisation and mergers.

(The North Africa Post)

30

Number of new branches of Kukito fast food outlets, Java House restaurant chain plans to open in Nairobi in the next five years, bringing more competition to quick-service eateries in Kenya's capital.

(Business Daily)

$100 million

Investment by the IFC in Egypt's first private sector green bond. Issued by Commercial International Bank (CIB), the country’s largest private bank, the bond will help CIB increase lending to businesses that want to invest in eco-friendly initiatives

(Daily News Egypt)

52%

Increase in the value of cash transactions executed via mobile phones in Kenya in the first six months of the year over the same period of 2021. The record value of $30 billion reflects the continued economic recovery after the Covid-19 lockdowns of last year.

(Business Daily)

3

Units proposed under Eskom's restructuring plans. The South African power company put out a call for financial advisors to support its unbundling into transmission, generation and distribution units to better manage its debt profile.

(Business Tech)

$3 million

Financing raised by B2B logistics platform Omnibiz to digitise supply chain management for informal retailers in Nigeria. The seed round will support the startup to expand its asset-light distribution model from four cities to six.

(Tech Crunch)

10,000

Investors in the initial public offering (IPO) of Tanzanian agribusiness firm, Jatu, on the Dar es Salaam Stock Exchange. Led by local investors, the IPO raised $7.6 million for the youth-led firm, which will be used to finance commercial farming and processing activities.

(Daily News)

75%

Kenya's share of tea sold via the Mombasa auction, highlighting the country's position as the leading exporter in the region. However, Rwandan tea ranks first in terms of price, at $2.46 per kilo compared to $2.07 per kilo for Kenyan tea.

(Business Daily)

$34 million

Injected into Africa's first renewable energy yieldco. UK Climate Investments has established this innovative green finance vehicle alongside Investec Bank Limited and Eskom Pension and Provident Fund. Managed by Revego, the initial portfolio comprises stakes in six projects located across South Africa.

(ESI Africa)

100 years

Production supported by resources at Kenmare Resources's titanium mineral mine in Mozambique at current rates of output. The company, which is one of the world's leading producers of titanium minerals, saw a 278% jump in profits in the first half of the year on the back of increased production and sales.

(Club of Mozambique)

56

Number of Massmart grocery stores in South Africa acquired by Shoprite's grocery unit, Checkers, in an $89 million deal. Walmart-owned Massmart is selling off its fresh food operations to focus on its better performing businesses as it seeks to return to profitability.

(Food Business Africa)

$2 billion

Value Chinese-backed African fintech start-up, OPay, after it raised a $400 million in a round led by SoftBank. The Series C raise is a record in Africa's tech scene and makes OPay the continent's third unicorn after Jumia and Flutterwave.

(Techcrunch)

1st

Protection Designation of Origin (PDO) certificate issued by the EU to an African product. South Africa's rooibos tea will now receive the same protection as Champagne, Porto, Queso Manchego and other iconic products, creating greater product recognition and demand.

(Food Business Africa)

162 MW

Generation capacity added to the Inga II hydropower plant on the Congo River with funding from Kamoa Copper SA and the DRC's power company. The upgrade will bring the plant's capacity to 240 MW. The Kamoa-Kakula Copper Mine will have priority access to the power generated, furthering its aim to be the greenest copper producer.

(ESI Africa)

Review by Kili Partners . Powered by Asoko Insight

The Federal Government of Nigeria has opened United Kingdom declaration facilities based in London for the Voluntary Offshore Assets Regularization Scheme (VOARS). This is the third facility after the Nigeria (based in Abuja) and Dubai facilities. Under the VOARS, pursuant to the Presidential Executive Order 008 2018 Amendment 2019, relevant persons or their intermediaries can regularize their residual (offshore) assets located anywhere in the world by the payment of a one-time levy. All proceeds from the VOARS are to be invested in infrastructure development through Nigeria Essential Infrastructure Fund (NEIF).

Relevant persons or their intermediaries (upon presentation of a valid power of attorney) may make declarations through any of the three facilities in Abuja, Dubai or London. Upon such declaration, the declarant will benefit from the government's permanent waiver of prosecution for offences related to the offshore assets voluntarily declared under Special Clearances and Non-Prosecution Agreements.

According to the Attorney-General and Minister of Justice, the declaration will also offer banks, asset managers, trusts and other intermediaries the opportunity to clean their books whilst regularizing undeclared assets under their custody. The Minister of Finance noted that in addition to the numerous benefits of the scheme, declarants and their custodian banks can also invest parts of the regularized assets and earn high returns whilst investing in the country's infrastructure development.

On 11 August 2021, Rwanda joined the Multilateral Convention on Mutual Administrative Assistance in Tax Matters, as amended by the 2010 protocol. The signing took place in Paris. The convention has now been signed by a total of 144 jurisdictions, following the signatures of Maldives, Papua New Guinea and Rwanda on the same date.

The Kenyan government enacted several tax amendments related to direct taxation including the deeming of family trust income as chargeable income. This income will, however, be exempt if the family trust is registered.

More details of the various amendments which unless otherwise indicated will apply from 1 July 2022 relating to direct taxation are as follows:

exempting the following from minimum tax:

persons whose retail price is controlled by the government;

persons engaged in insurance business;

persons engaged in manufacturing businesses whose cumulative investment from 2017 to 2021 is at least KES 10 billion; and

persons engaged in distribution businesses whose income is wholly based on a commission and persons licensed under the Special Economic Zones Act;

family trust income is deemed as income chargeable to income tax;

applying an income tax exemption to registered trusts on:

any amount that is paid out of the trust income on behalf of any beneficiary and is used exclusively for the purpose of education, medical treatment or early adulthood housing;

income paid to any beneficiary which is collectively below KES 10 million in the year of income; and

such other amount as the Commissioner General of the Kenya Revenue Authority (Commissioner) may prescribe from time to time;

exempting the transfer of property to a family trust from capital gains tax;

exempting registered family trusts from income tax;

introducing withholding tax on deemed disbursements to trust beneficiaries at a rate of 25% except where such income is exempt from tax; and

the new limitation of interest deductibility rule, which will take effect on 1 January 2022, will not apply to banks or financial institutions licensed under the Banking Act or to micro and small enterprises registered under the Micro and Small Enterprises Act 2012. This rule limits the deductible interest expense to 30% of the earnings before interest, taxes, depreciation and amortization (EBITDA;

the double taxation agreements or arrangements shall be subject to the Treaty Making and Ratification Act 2012;

extending the transitional period on capital allowances claimable relating to capital expenditure for bulk storage and handling facilities supporting the Standard Gauge Railway to 31 December 2022;

reintroduction of the definition of farm works with effect from 1 January 2022. "Farm works" means "farmhouses, labourers quarters, any other immovable building necessary for the proper operation of the farm, fences, dips, drains, water and electricity supply works and other works necessary for the proper operation of the farm". The Finance Bill 2021 had only proposed a review of the definition of "manufacture" and reintroduced a definition of "civil works" to include:(i) roads and parking areas; (ii) railway lines and related structures; (iii) water, industrial effluent and sewerage works; (iv) communications, electrical posts, pylons and other electrical supply works; and (v) security walls and fencing; and

introducing investment deductions at 100% with effect from 1 January 2022 where:

the investment value outside Nairobi City County and Mombasa County in that year of income is at least KES 250 million;

a person has invested in a special economic zone; and

the cumulative investment value in the preceding 3 years outside Nairobi City County and Mombasa County is at least KES 2 billion: Provided that where the cumulative value of investment for the preceding 3 years of income was KES 2 billion on or before 25 April 2020, and the applicable rate of investment deduction was 150%, that rate shall continue to apply for the investment made on or before 25 April 2020.

Dubai Customs launched a comprehensive guide for all the services and facilities it provides to enable traders and businesses, which selected Dubai as their preferred investment destination, increase their trade and boost their revenues. The guide will be introduced to the participants and exhibitors of EXPO2020 Dubai.

Within the national efforts and preparations to fulfil the requirements of the bold plans and agendas including the UAE Centennial 2071 and the 50th year Jubilee, Dubai Customs has built a sophisticated smart network of channels that adds a big value to any business activity. These included the Smart EXPO2020 Customs Channel, dedicated to serve the exhibitors of the global event. The Channel was part of the UAE’s nomination portfolio in 2013 to host EXPO2020 in Dubai. Customs centers at Jebel Ali and Al Maktoum International Airport will help complete all EXPO’s customs transactions around the clock to ensure streamlined and quick customs processes, saving the exhibitors time and cost following the directions of His Highness Sheikh Mohammed Bin Rashid Al Maktoum, Vice President, Prime Minister and Ruler of Dubai.

“The Smart EXPO Customs Channel will facilitate all customs transactions for the participants in EXPO2020 Dubai,” said H.E. Ahmed Mahboob Musabih, Director General of Dubai Customs. “We have many outstanding services that can help advance trade and investments including the Authorized Economic Operator (AEO) program, which was launched at the federal level to enhance external trade. There are now 80 companies’ members in the AEO whose external trade reaches AED20 billion. Dubai Customs has also launched the Cross Border e-Commerce platform to lure more business and investments into the emirate. It is the first of its kind in the region and it aims to raise businesses’ share in e-commerce local and regional e-commerce to AED24 billion by 2024. Participants can now benefit from the second phase of the iDeclare App and the AI potential it has. The app enables users learn about the commodities they need to declare, simply by taking a photo of the item, which will then show the HS Code and any customs charges required. Users can also learn about the services and amenities available at Dubai International Airport, including restaurants, free zone, exit gates and others. The app helps passenger pass through the red lane and complete their customs transactions in less than 4 minutes.

“All these facilities will not compromise on security. We have in place a number of advanced systems and programs that will help further secure the borders and streamline trade activity. These include the Smart Risk Engine, the Smart Auditing System, the Integrated B2G Business Channel and the Smart Workspace. These sophisticated systems will help ensure 97.8% of customs transactions completed automatically without any human intervention.”

Last May, Dubai Customs organized the 5th WCO Global AEO Conference in cooperation with the World Customs Organization and the UAE Federal Customs Authority. The conference saw participation of around 100 speakers and 12,000 specialists from 160 countries who confirmed the importance of enhanced cooperation and coordination between customs administrations, government departments and the private sector. It was the first AEO conference to be held in the region.

Dubai showed quick recovery from the repercussions of Covid-19 in different economic sector thanks to the resilient strategies and plans the emirate followed in the face of the pandemic, and the dynamic and wise initiatives directed by His Highness Sheikh Mohammed Bin Rashid Al Maktoum, Vice President, Prime Minister and Ruler of Dubai.

Trade sector continued its growth exceeding the pre-Covid-19 period. Customs transactions completed by Dubai Customs reached 11.2m transactions in the first half of 2021 staggeringly growing 53.4% from 7.3m transactions in the corresponding period in 2020. This reflects a versatile and resilient economy that is able to absorb severe shocks like that caused by the pandemic.

It also reflects the vital role Dubai plays as a global trade hub and the resilience of its infrastructure and systems in dealing with tough challenges including covid-19.

“Dubai is leading the global recovery way. The emirate’s non-oil external trade grew 10% to AED354.4b in Q1, 2021, from AED323b in the corresponding period in 2020,” said H.E. Ahmed Mahboob Musabih, Director General of Dubai Customs. “We work with all our energy to develop systems and programs that speed up the completion of transactions and the flow of foreign trade movement in the Emirate. This comes as part of our quest to realize the vision of His Highness Sheikh Mohammed Bin Rashid Al Maktoum, Vice President, Prime Minister and Ruler of Dubai to hit the 2 trillion milestone in external trade.

“Trade sector in Dubai plays a pivotal role in supporting the economy. We work hard in Dubai to ensure the continuous success of this sector, helping Dubai maintain its leading global position as a global hub for business and investment. We developed several programs and plans to facilitate trade including the recent ‘Electronic Confirmation of Exit/Entry’ initiative, which was launched in cooperation with DP World, UAE Region. The project eases the process of refund claims submission at Dubai Customs, saves time and cost, while further expediting the exports of all kinds of goods.

“Dubai Customs has launched 24 initiatives, which are dedicated to serve the visitors and exhibitors of EXPO2020.The initiatives are fully integrated with other government partners’ systems.”

Dubai Customs completed 11.16 million transactions through smart and electronic channels (99.6%). Around 7.9 million customs transactions (70.8%) were completed through smart channels, 3.2 million (28.8%) through electronic channels, and only 41,800 (0.37%) transactions were done manually.

“The World Customs Organization sees us as an example to be followed by other customs organizations, thanks to the outstanding projects and initiatives we develop to serve the global customs sector. Our recent hosting of the 5th WCO Global Authorized Economic Operator Conference indicates that the business world has much trust in the emirate as a leading hub for trade, and reflects the major role it plays in facilitating global trade, and the close and fruitful relationship between Dubai Customs and the World Customs Organization,” said Musabih.

The Conference presented an important forum for the exchange of ideas and insights between trade and supply chain professionals and officials, and brought together all stakeholders of global trade to explore the challenges, opportunities, and way forward for global trade under the Authorized Economic Operator programme.

Customs declarations rose 66.6% in the first 6 months of this year to reach 10 million declarations compared to 6 million declarations in the corresponding period in the previous year. This means more than 55,500 declarations a day in average. This big figure would not have been achieved without the outstanding technological structure in place including the advanced Smart Workspace, which helped complete a declaration in 4 minutes in average.

The transactions also included 475,900 claim requests, 298,000 certificate and report requests, and 139,800 customs inspection date booking requests, and 110,600 business registration requests.

DMCC – the world’s flagship Free Zone and Government of Dubai Authority on commodities trade and enterprise – today announced it recorded its best August on record since its establishment in 2002, with 204 new member companies registered, and best eight-month performance in seven years. This builds on the business district’s record-breaking success in recent months, with strong performance in the first half of the year, during which it welcomed 1,230 companies, the best 6-month performance since 2013.

DMCC has witnessed persistent growth over the years, supported by strategic partnerships that enhance the ease of doing business, roadshows that attract trade flows to Dubai and new launches, including its latest DMCC Crypto Centre – a comprehensive ecosystem for businesses operating in the cryptographic and blockchain sectors.

Ahmed Bin Sulayem, Executive Chairman and Chief Executive Officer, DMCC said: “DMCC continues to edge closer to the target we set ourselves – to reach 20,000 members by the end of 2021. The record-breaking level of business activity, even during the quieter summer months, reflects the continued appeal of our business district to companies of all sizes and origins. As Dubai prepares to welcome the world to EXPO 2020 Dubai in a few weeks, we see a wealth of opportunities on the horizon. Building on this momentum, we are looking forward to the next few months which will undoubtedly be marked by many more milestones and achievements.”

Ahmad Hamza, Executive Director – Free Zone, added: “I am incredibly proud of the DMCC’s record-breaking performance. The ecosystem we offer, our fully digitalised set up process, along with the innovative solutions, products and services we bring mean we remain the business community’s partner of choice.Our network is unmatched and with that comes unique connectivity – these are pre-requisites for any company seeking growth.”

China will adopt multiple measures to stabilize manufacturing investment, the country's top economic planner said Tuesday.

The country will boost green investment by encouraging investment in technological upgrading and stepping up policy support for the traditional manufacturing industry to reduce carbon emissions, said Meng Wei, spokesperson for the National Development and Reform Commission.

The country will also support investment in advanced manufacturing and improving weak links in the industrial and supply chain, Meng added.

Comprehensive measures will be taken to ease the upward pressure on commodity prices and strengthen investment incentives for middle and downstream manufacturing enterprises while implementing various cost reduction policies, the spokesperson said.

China's fixed-asset investment amounted to 30.25 trillion yuan (about 4.67 trillion U.S. dollars), up 10.3 percent year on year in the first seven months of this year, data from the National Bureau of Statistics showed.

Specifically, investment in manufacturing gained 17.3 percent year on year during the period, the data showed.

Putting on a helmet and sitting in front of several big screens, you are able to experience the exciting moment of a spacecraft launch. This is one of the highlights of the 2021 Global Digital Economy Conference that concluded in Beijing Tuesday.

During the two-day event that opened on Monday, cutting-edge technologies featuring data-driven innovation were displayed while participants focused on discussions concerning the digital economy as a new driver of China's economic growth despite the COVID-19 pandemic.

China's digital economy kept a high growth rate of 9.7 percent in 2020 amid the pandemic and global economic downturn, according to a white paper released by the China Academy of Information and Communications Technology (CAICT).

The country's digital economy scale hit 39.2 trillion yuan (about 6.1 trillion U.S. dollars) last year, accounting for 38.6 percent of the GDP.

"As people are more connected than ever due to the increasingly diversified communication means, we have all benefited from the progress of digitalization, especially during the hardest time of the pandemic," said Guido Giacconi, vice-president of the European Union Chamber of Commerce in China.

The digital economy has become a key to achieving economic recovery and promoting sustainable development with the global economy, which is still in a fragile state of recovery, said Zhuang Rongwen, director of the Cyberspace Administration of China, at the opening.

The digital economy has displayed strong resilience in the face of the pandemic, as it gives a strong boost to a number of new business models such as online shopping and education, telemedicine and artificial intelligence, said Cai Fang, an expert with the Chinese Academy of Social Sciences.

China has built the world's largest optical fiber and 4G and 5G mobile broadband networks, with the number of 5G terminal connections exceeding 365 million and 5G application scenarios becoming increasingly rich, said Xiao Yaqing, minister of industry and information technology.

With its digital economy ranking second in the world, China has highlighted the digital economy development in its 14th Five-Year Plan (2021-2025) to build a digital China.

Chinese companies will also be encouraged to tap opportunities in the overseas digital market in the following decade, said Lei Jun, chairman of Xiaomi Corporation, a Chinese smartphone manufacturer.

According to a guideline jointly released by Chinese government departments on July 23, more efforts will be made to enable domestic digital economy enterprises to accelerate their deployment of overseas research and development centers and product design centers and strengthen cooperation with overseas technology companies in fields such as big data, 5G and artificial intelligence.

The capital city Beijing has also introduced an action plan Monday on accelerating the process of building itself into a worldwide pioneer in digital economic development.

As noted in the plan, the added value of Beijing's digital economy is expected to account for about 50 percent of its GDP by 2025. Last year, the added value of the city's digital economy has exceeded 1.44 trillion yuan, accounting for about 40 percent of its total economic volume.

The World Trade Organization predicts that digital technologies will promote an annual growth of the global trade volume by around 2 percentage points by 2030, and the proportion of global service trade will be increased from 21 percent in 2016 to 25 percent by then.

"In face of the challenges such as sluggish economic growth and aging society, the digital economy will enable an inclusive high-quality development that enables more elderly people to overcome the digital divide," said Cai.

Shanghai municipal government released on August 24, 2021 the Development Plan of Shanghai International Financial Center in the 14th Five-year Plan Period, which contains 44 policy measures.

The plan proposed to enhance business climate for financial services and create a sound financial ecosystem. Financial lease firms and commercial factoring companies are encouraged to be connected to the central bank's credit reference system; the city will support Dishui Lake to build a financial bay, Lingang New Area to play a helpful role for integrating onshore and offshore financial services, and Hongqiao to optimize trade financing services. The plan also proposed to reinforce financial support to key sectors like electronic information, life science, automobile, high-end equipment, and new materials.

On 30 July 2021, the State Taxation Administration (STA) announced on the Matters Regarding Application of the Simplified Procedures for Unilateral Advance Pricing Arrangements (State Taxation Administration Announcement [2021] No. 24, hereafter “No.24”). Relying on the advance pricing arrangement (APA) framework set out in the Announcement of the State Taxation Administration on Issues to Improve Administration of Advance Pricing Arrangements (State Taxation Administration Announcement [2016] No. 64, hereafter “No.64”), the STA has further simplified the procedures for unilateral APAs, valid from 01 September 2021.

Highlights of No. 24-Simplify the Procedures and Set a Time Limit

No. 64 regulates that the APA process consists of the following six phases: (i) pre-filing meeting, (ii) intention for an APA, iii) analyses and evaluation, (iv) formal filing, (v) negotiations and signing, and (vi) monitor and execution (collectively referred as "general procedures"). The simplified procedures contain three phases, namely (i) evaluation of application, (ii) negotiation and signing, and (iii) monitor and execution. The pre-filing meeting and other phases are exempted.

The simplified procedures set clear processing time limits for tax authorities on the acceptance of APA applications, and the negotiation and signing. Tax authorities must send a Notice on Tax Matters to the submitting enterprise within 90 days of receiving the APA application to inform the enterprise of whether or not the application has been accepted. The in-charge tax authorities must complete the negotiation within six months of issuing the Notice of Tax Matters to the enterprise accepting the application. During the negotiation, any time spent by the enterprise on preparation and submission of additional information required by the tax authorities is not included in the six month period. As such, if the related documents are fully-prepared in advance and submitted by the enterprise in time, a unilateral APA application could be concluded within six to nine months under the simplified procedures[1]. Unilateral advance pricing arrangements shall apply to related party transactions in the period of three to five years from the tax year following the date of service of the "Notice on Tax Matter" on the enterprise by the tax authorities in charge for acceptance of application.

The left column of the following table shows the two applicable conditions, both of which must be met for using the simplified procedures. The right column of the table also shows the circumstances under which the tax authorities may reject an application and when the simplified procedures are temporarily not applicable.

Table: Application Conditions and Rejection Circumstances of the Simplified Procedures for Unilateral APAs

Observations and Recommendations

APAs are arrangements reached between enterprises and tax authorities, or between two tax authorities, with respect to the pricing principles and calculation methods for related-party transactions. It is an important tool for enterprises to obtain transfer pricing and tax certainty for cross-border business operations, and it plays an important role in reducing multinational enterprises' transfer pricing compliance costs and in promoting enterprises' cross-border investments and operations. No. 24 announces simplified procedures for unilateral APAs, improving the efficiency of APA negotiation and signing by simplifying the phases of the application and specifying time limits.

Based on our practical experience, we consider that enterprises should focus on the following aspects:

Time limits – This is the first time that APA regulations have specified timeline requirements for tax authorities, where decisions on whether or not to accept the APA application must be made within 90 days and negotiation and signing must be completed within six months. This will help enterprises and tax authorities complete the entire unilateral APA negotiation and signing process within a shorter period. We believe that such time limits requirement may reduce enterprises' concerns on the relatively time-consuming process of APA negotiation and signing.

Applicable conditions — When evaluating whether an enterprise meets the applicable conditions for the simplified procedures, the enterprise may proactively plan to meet the requirements. For example, an enterprise that is exempt from preparing the contemptuous transfer pricing documentation may consider obtaining the application by preparing and submitting the contemporaneous transfer pricing documentation for the latest three tax years to tax authorities.

Applicable to unilateral APAs — While there are advantages, the simplified procedures do not change the effect of unilateral APAs. If both parties in the cross-border related-party transaction want to obtain tax certainty and reduce double taxation risks more effectively, we recommend applying for bilateral APAs in accordance with the general procedures under No. 64.

Before, STA shall involve in each case of Unilateral Advance Pricing Arrangement, which objectively makes the number of arrangements signed can not meet the actual needs of enterprises. With the formally establishment of the Simple Procedures for Unilateral Advance Pricing Arrangement, STA delegates the executive power to competent tax authorities of enterprises, which can improve the ability to process applications. Thus, it can help enterprises effectively avoid or eliminate double taxation and achieve CIT certainty in transfer pricing arrangements.

We recommend that taxpayers with cross-border related-party transactions should actively understand the simplified procedures for unilateral APAs, one of the most critical measures of improving the business environment in the field of taxation, and should communicate and discuss internally. Enterprises may leverage this new policy to gain tax certainty in a more time-efficient and cost-effective way.

[1] The time to completion is expected to be significantly shorter under the new regulations. According to the 2019 China Advance Pricing Arrangement Annual Report published in October 2020, the STA signed 101 unilateral APAs between 1 January 2015 and 31 December 2019, most of which were completed within 2 years, with 52.48% completed within 1 year, 36.63% within 1 to 2 years, and 10.89% over 2 years.

The State Administration for Market Regulation and the State Taxation Administration issued a joint circular on August 3, 2021 to clarify matters related to simplified deregistration of enterprises, so that small, medium-sized and micro firms can exit the market more easily.

According to the circular, the scope of simplified deregistration will be expanded to companies that have no creditor's rights or debts such as outstanding expenses for settlement, employee wages, social insurance premiums, statutory compensation, taxes (late fees or fines) payable, etc. All the investors shall make a written commitment to assume legal liability for the authenticity of the above situation. Through information sharing, tax authorities shall verify the relevant tax-related information under the prescribed procedures and requirements. Tax authorities will raise no objection if the taxpayer is shown to fall under any of the following circumstances upon the inquiry system:

it is a taxpayer that has never handled tax-related matters;

it is a taxpayer that has handled tax-related matters but has never received or used invoices (including invoices issued on a commission basis), has no tax in arrears or has no other pending matters;

it is a taxpayer that has completed tax clearance formalities, such as the handing in of invoices and the settlement of tax payable, at the time of inquiry.

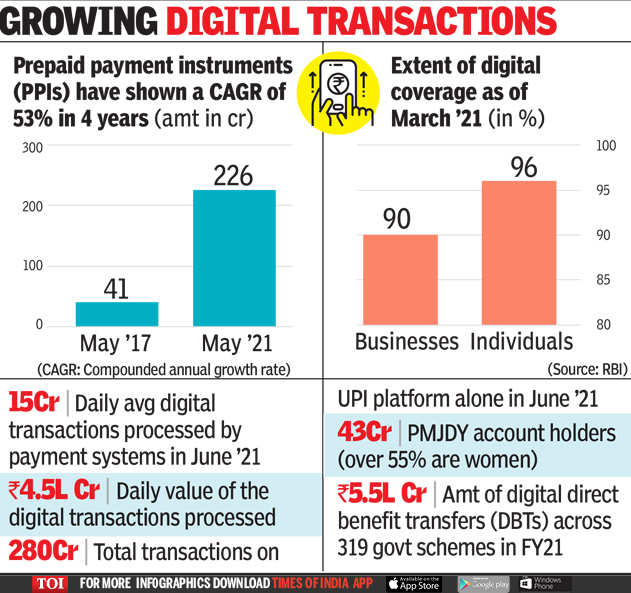

The Reserve Bank of India (RBI) has said that there was a 24% improvement in financial inclusion (FI) as measured by RBI’s FI-Index between March 2017 and March 2021.

MUMBAI: The Reserve Bank of India (RBI) has said that there was a 24% improvement in financial inclusion (FI) as measured by RBI’s FI-Index between March 2017 and March 2021.

The FI-Index incorporates details of banking, investments, insurance, postal as well as the pension sector in consultation with government and respective sectoral regulators. In April this year, the RBI had announced that it would launch the FI-Index to capture the extent of financial inclusion.

On Tuesday, the RBI announced the first numbers of the FI-Index, and will henceforth publish the data once a year in July. The highest weightage in the index (45%) is given to the usage of various financial services, followed by access (35%) and quality (20%).

The index captures information on various aspects of financial inclusion in a single value, ranging between 0 and 100, where 0 represents complete financial exclusion and 100 indicates full financial inclusion.

One of the biggest drivers of financial inclusion in the country has been the Pradhan Mantri Jan Dhan Yojana (PMJDY). There are about 42.6 crore PMJDY account holders with more than 55% being women. While the JDY was launched in 2014, the usage of the accounts picked up with the increase in direct benefit transfers (DBTs), which were facilitated by digital platforms and Aadhaar.

The impact of the digital payment in DBT can be discerned from the fact that Rs 5.5 lakh crore was transferred digitally across 319 government schemes spread over 54 ministries during 2020-21.

Since the pandemic, financial inclusion got a boost due to the increased usage of digital platform by small merchants and peer-to-peer payments.

“Lessons from the past and experiences gained during the Covid pandemic clearly indicate that financial inclusion and inclusive growth reinforce financial stability,” RBI governor Shaktikanta Das had said, speaking at the financial inclusion summit.

“As of March 2021, banks have achieved a digital coverage of 95.9% of individuals, while the achievement for businesses stood at 89.8%,” Das said in the summit.

The rise of the fintech’s have also supported financial inclusion as they innovated to simplify and promote digital payments like the UPI (Unified Payments Interface).

According to a report by Macquarie, while the retail payments (by value) have grown at an 18% CAGR over FY15 to ’21, UPI has grown at a CAGR of around 400% over FY17-21 and now forms 10% of overall retail payments (excluding RTGS) from 2% seen couple of years ago.

“Despite being a late entrant, UPI’s FY21 annual throughput value of around Rs lakh crore was almost 2.8x that of credit and debit card (at POS) combined largely,” the report said.