2021 Mid-Year Export Review: Robust But Uneven Recovery

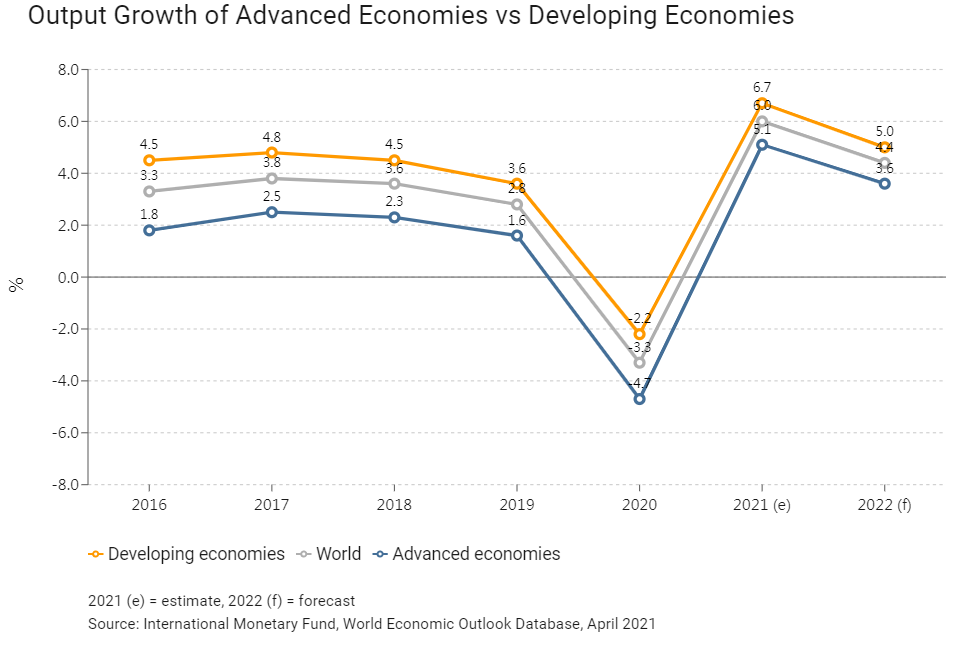

Hong Kong’s exports showed a sharp rebound of 30.8% year-on-year in the first four months of 2021, along with strong growth of 10% in global trade during 1Q21. This was largely on account of subsiding pandemic restrictions and increasingly aggressive monetary and fiscal stimuli in many of the major economies. According to the International Monetary Fund (IMF), global economic growth is projected to be 6% this year and 4.4% in 2022, while the World Trade Organization (WTO) is forecasting 8% growth in world trade volume in 2021. Given the threat of the new coronavirus variants and the shortage of vaccines in less-developed economies, however, any global economic recovery is likely to be highly uneven, with the situation also being exacerbated by tense China-US relations and other geopolitical uncertainties. With a reading of 48.7 points, the latest HKTDC Export Index has, however, indicated that exporter sentiment has continued to improve across major sectors and markets, with the figure well up on the record low of 16 points in 1Q20. As a consequence, in view of the improving sentiment and strong export performance, HKTDC Research has revised its 2021 export growth forecast to 15% from 5%, albeit from a relatively low comparison base.

More than a year on since the start of the pandemic, the economic performance of many of the major economies remains highly uneven and unsteady. While some economies are effectively reining in any new cases and, consequently, undergoing a faster economic recovery, some are still ramping up their containment measures amid a local resurgence of the pandemic. With relatively effective containment measures and massive fiscal support, Hong Kong’s real GDP resumed appreciable year-on-year growth of 7.9% in 1Q21, bringing to an end six consecutive quarters of contraction. During the same period, the mainland’s GDP picked up by 18.3%, while the US’s increased marginally by 0.4%. The GDPs of the EU and Japan, however, contracted by 1.7% and 5.1%, respectively.

|

2019 |

2020 |

January-April 2021 |

||||

|

HK$ mn |

Growth % |

HK$ mn |

Growth % |

HK$ mn |

Growth % |

|

| Total Exports |

3,988,685 |

-4.1 |

3,927,517 |

-1.5 |

1,492,087 |

+30.8 |

| Domestic Exports |

47,751 |

+3.1 |

47,442 |

-0.6 |

27,182 |

+100.7 |

| Re-exports |

3,940,935 |

-4.2 |

3,880,075 |

-1.5 |

1,464,905 |

+30.0 |

| Imports |

4,415,440 |

-6.5 |

4,269,752 |

-3.3 |

1,591,200 |

+25.5 |

| Total Trade |

8,404,126 |

-5.4 |

8,197,270 |

-2.5 |

3,083,287 |

+28.0 |

| Trade Balance |

-426,755 |

-342,235 |

-99,113 |

|||

| Source: Hong Kong Trade Statistics, HKSAR Census and Statistics Department | ||||||

|

2019 |

2020 |

January - April 2021 |

||||

|

HK$mn |

Growth % |

HK$mn |

Growth % |

HK$mn |

Growth % |

|

| US |

304,004 |

-14.8 |

258,842 |

-14.9 |

83,898 |

+19.9 |

| EU(27)(1) |

306,168 |

-7.5 |

280,207 |

-8.5 |

97,516 |

+20.2 |

| Japan |

121,012 |

-6.4 |

109,326 |

-9.7 |

35,393 |

+1.5 |

| Developing Asia |

2,862,040 |

-3.1 |

2,920,350 |

+2.0 |

1,128,982 |

+32.8 |

| Mainland China |

2,210,854 |

-3.3 |

2,324,511 |

+5.1 |

893,441 |

+34.2 |

| ASEAN |

310,732 |

+0.8 |

282,941 |

-8.9 |

103,080 |

+11.9 |

| Latin America |

79,898 |

+1.4 |

66,225 |

-17.1 |

26,590 |

+31.0 |

| Middle East |

86,581 |

+4.8 |

83,553 |

-3.5 |

31,582 |

+19.4 |

| Emerging Europe |

90,022 |

-7.6 |

92,325 |

+2.6 |

32,155 |

+20.5 |

| Africa |

42,657 |

-0.3 |

45,172 |

+5.9 |

15,850 |

+32.1 |

| Note (1): Hong Kong trade with the EU has excluded the post-Brexit UK since February 2020. | ||||||

| Source: Hong Kong Trade Statistics, HKSAR Census and Statistics Department | ||||||

|

2019 |

2020 |

January - April 2021 |

||||

|

HK$ mn |

Growth % |

HK$ mn |

Growth % |

HK$ mn |

Growth % |

|

| Electronics |

2,725,844 |

-4.1 |

2,819,804 |

+3.4 |

1,068,843 |

+32.8 |

| Precious Jewellery |

62,867 |

+10.4 |

50,335 |

-19.9 |

22,694 |

+62.6 |

| Clothing |

96,225 |

-11.3 |

63,784 |

-33.7 |

18,263 |

-2.3 |

| Watches & Clocks |

64,223 |

-3.2 |

46,386 |

-27.8 |

17,627 |

+28.1 |

| Toys |

34,918 |

-27.4 |

29,628 |

-15.1 |

8,972 |

+42.7 |

| Household Electrical Appliances |

15,476 |

+1.9 |

13,891 |

-10.2 |

4,500 |

+15.9 |

| Source: Hong Kong Trade Statistics, HKSAR Census and Statistics Department | ||||||

Mainland China Takes the Lead

While the pandemic undoubtedly triggered a severe global recession in 2020, it is also fair to say that effective containment measures limited the extent of the economic downturn in mainland China. In fact, the mainland’s GDP rose by 2.3% in 2020, making it one of the few economies in the world to register growth. For the first four months of 2021, there has also been every sign that this upward momentum is likely to be sustained. Looking more generally to the future, economic growth in a number of the advanced economies has begun to resume following the gradual relaxation of local lockdowns and other containment measures. Typically, business activities are slowly returning to pre-pandemic levels, with many governments providing fiscal support to designated business sectors in order to stimulate economic growth. Elsewhere, though, especially among the developing nations, economic recovery has been hindered by a resurgence of coronavirus infections and limited access to vaccines. Now, as well as the negative legacy of the pandemic, many developing economies may have to contend with the additional challenges of an overall tightening in global financial conditions and fluctuations in external demand. In April the IMF estimated the global economy would rebound by 6% in 2021, with an anticipated vaccine-driven recovery in the second half of the current year, before moderating to growth of 4.4% in 2022.

Key Risks: Pandemic Resurgence and Trade Protectionism

The re-emergence of Covid-19 and the potential spread of new variants are seen as the key risks for many economies, particularly in the case of less-developed nations or those with limited access to vaccines and related medical supplies. Inevitably, this will lead to continued uncertainty with regard to the global economic recovery, while also hindering the revival of global demand to a certain extent. As reported in the latest HKTDC Export Index, 41.5% of exporters see the pandemic as a primary concern in the near term, followed by weakened global demand (16.7%). In addition, concerns relating to the global supply chain disruptions triggered by the pandemic and rising trade protectionism – most notably the prolonged China-US trade dispute – have prompted some companies to rethink their sourcing and manufacturing networks, including relocating manufacturing facilities back home or shifting their sourcing operations to other Asian countries. As the trade talks between China and the US were stalled by the pandemic following January 2020’s phase-one trade agreement, little progress has been made towards resolving the issue. There have also been concerns that even this phase-one deal has yet to be fully implemented. Under the terms of phase one, China agreed to buy at least US$200 billion more US goods and services (relative to 2017 levels) before the end of the two-year agreement in December this year. According to estimates from the US-based Peterson Institute for International Economics, however, China’s purchase of US goods fell short by more than 40% in 2020. Furthermore, in the first four months of this year, China’s purchases of US goods represented just 60% of the year-to-date target. While it is still unclear how the two economies will manage their trade conflict, the risk to Hong Kong seems tilted more to the downside. Should mainland China purchase more products from the US, it will have only limited impact on Hong Kong’s trade, largely because mainland imports of US goods largely take the form of direct shipments. For 2020 overall, mainland China imported US$134.9 billion of goods from the US and, of that, just 7.9% (about US$10.7 billion) was routed via Hong Kong. Regardless of this, though, should China-US trade tension worsen, Hong Kong exporters may suffer on account of the deteriorating sentiment and growing uncertainty, a trend that has been evident in the past two years.Hong Kong Exports: Strong Recovery From a Low Base

Given the improving economic outlook in the major markets and the generally more stable trading environment, we remain optimistic as to Hong Kong’s performance in the latter half of this year. Accordingly, HKTDC Research has revised its 2021 Hong Kong export performance forecast upward to 15% from 5%, while acknowledging it is from a low base. This is, potentially, the highest level of growth since 2010 when exports surged by 22.8% in the post-global financial crisis recovery period.

With regard to individual major industry sectors, electronics – which accounts for 70% of Hong Kong’s total exports – regained much of its growth momentum in the first four months of 2021. This is partly because, although many of the Covid-related lockdown and social-distancing measures have been lifted, work-from-home / e-learning arrangements have become the new normal for many office workers and students. As a result, some companies have adopted a hybrid model, allowing staff to split their work time between the home and office while, similarly, many students are now opting to take online courses after school in order to save on commuting time. The upshot of this is that demand is continuing to grow for electronics items such as computers, webcams, microphones and medical devices.

Less upbeat, however, is the outlook for the clothing sector. The continued relocation of production facilities to South and Southeast Asian countries, in tandem with depressed consumer demand, has resulted in a tough environment for Hong Kong’s clothing exporters. Regardless of this, there are a number of clear new product trends – most notably, multi-purpose and athleisure wear is on the rise as people are becoming more health conscious and keen to engage in different indoor and outdoor physical activities.

It is a very different picture with regard to Hong Kong’s toy exports, which surged by 42.7% in the first four months of 2021. Looking at this in more depth, exports of electronic and video games were up by 66%, while exports of more traditional toys and games climbed by 28%. Over the coming summer, a number of new 3D live-action and computer-animated movies are scheduled to be released, which is expected to boost demand for related digital games and peripheral toy products. In addition, the growing popularity of electronic gadgets and e-sports products / equipment is also seen as a potential driver of Hong Kong’s toy exports.

In the watches and clocks sector, although Hong Kong remains one of the world’s key exporters, in order to stay competitive, it is believed it will be necessary for the industry to move upmarket. In line with this, many of the city’s clock / watch makers are looking to develop locally designed and produced mechanical movements, while considering beginning the mass production of chronometers. At the same time, growing demand for smartwatches is seen as likely to continue to drive exports, especially as many consumers are thought to be more concerned about digitally monitoring their health in the wake of the pandemic.

Finally, turning to Hong Kong’s jewellery exports, these are also expected to pick up dramatically in line with the ongoing economic recovery. In particular, it is thought that demand for high-end jewellery items and related components – such as articles of goldsmith / silversmith ware, pearls and semi-precious stones – will rebound as consumer sentiment continues to improve. At the more affordable end of the scale, sales of stylish fashion jewellery, designer pieces and wedding / special occasion items are also expected to perform well.

Source: HKTDC